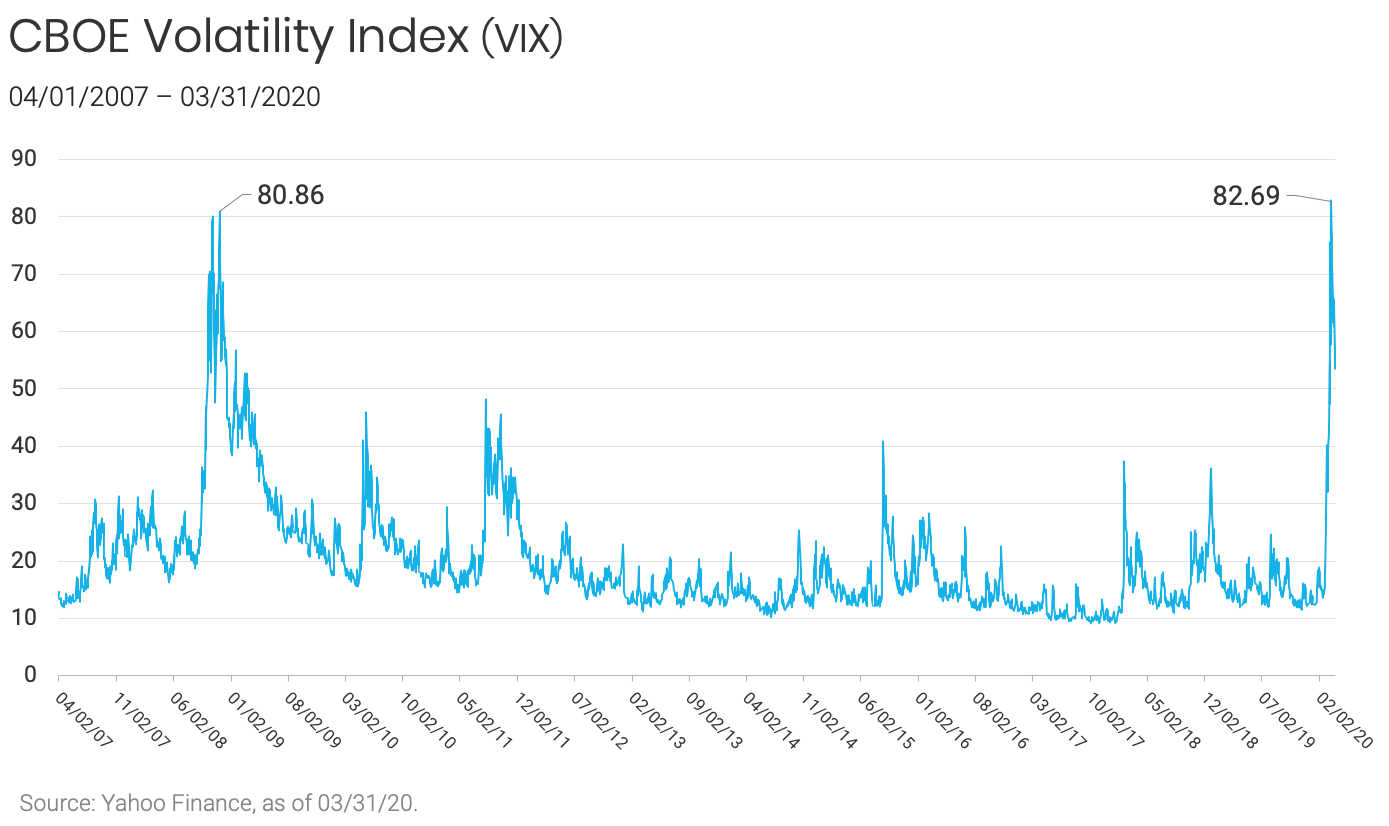

Due to increased global health and economic concerns regarding the COVID-19 pandemic, which is only further amplified by a global oil-price war and heightened political unrest regarding the upcoming U.S. presidential election, the CBOE Volatility Index (VIX) is trading at levels we haven’t seen since the global financial crisis over 10 years ago. While it is difficult for us to speculate on the potential significance of a sustained outbreak over the longer term, a variety of health precautions and travel restrictions are already in place, so you can only assume that there will be an impact to small and large public and private companies alike.

That said, this isn’t the first time we have seen an increase in market volatility or heightened health and safety concerns. Many of us have lived through a number of these cycles, such as outbreaks of Ebola, avian flu, SARs and MERs, the savings and loan crisis, the dot-com bubble, 9/11, the 2008 global financial crisis, and more. That is not to make light of the current environment as this COVID-19 is clearly a pandemic of significant proportions, but it’s an important reminder that our markets and economy have endured periods of sustained, heightened volatility before. It is also encouraging to see that both central banks and governments are taking aggressive measures to create various forms of stimulus to help combat this crisis.

As we continue to learn ways to persevere through this unprecedented time, we have seen that many of the innovative solutions the world is now turning to for business continuity, supply chain optimization, delivery services, life sciences technology, digital health, and vaccine development are coming from the VC asset class, and we believe some companies are well positioned to potentially thrive in circumstances like this. The SharesPost 100 Fund provides access to some of these exceptional private companies that are having a global impact, even through this pandemic.

Furthermore, private companies tend to involve far less short-term volatility compared to publicly traded companies, which are subject to rapid price changes from market forces that may not reflect underlying company fundamentals. That is not to imply that private companies themselves are immune to the same risks that publicly traded companies face, but rather that such companies may be affected less by short-term, idiosyncratic market volatility.

So, what does this all mean for late-stage private companies? First, it’s important to note that cash reserve levels in the VC asset class are at record highs on an absolute basis. We expect that capital will continue to be deployed, albeit at a slower pace and perhaps with more stringent requirements. Second, we believe companies have been prepping for a potential pullback well before this outbreak, as many VCs have been instructing their management teams to focus on more sustainable revenue growth, lowering cash burn rates, and trying to accelerate the path to profitability following some of the debacles witnessed in 2019.

Accordingly, although private companies are subject to the same risks from COVID-19 as the broader market and are at risk of losses of revenue and/or value, which may be substantial, we expect there to be only a limited increase in the volatility of the pricing of such companies in the near term. If there is a sustained period of increased volatility, then we may see a lag-effect impact, but we believe the impact would unlikely reach the magnitude of public market gyrations. The most meaningful input in valuing private company securities is typically the last round valuation (a company’s value after receiving their most recent round of equity funding), although the valuation of such companies also is affected by broader market forces and significant events, including macro events such as the impacts of COVID 19 and mitigation measures on such companies’ businesses. This dynamic is exhibited in the low correlation metrics of private markets with public markets. That said, for the foreseeable future we may potentially see less up-round financings (where a company’s worth increases in value after a financing round) and more protective provisions for preferred stockholders as investors gain negotiating leverage during these cycles. We had already started seeing signs of this valuation trend evolving during the second half of 2019.

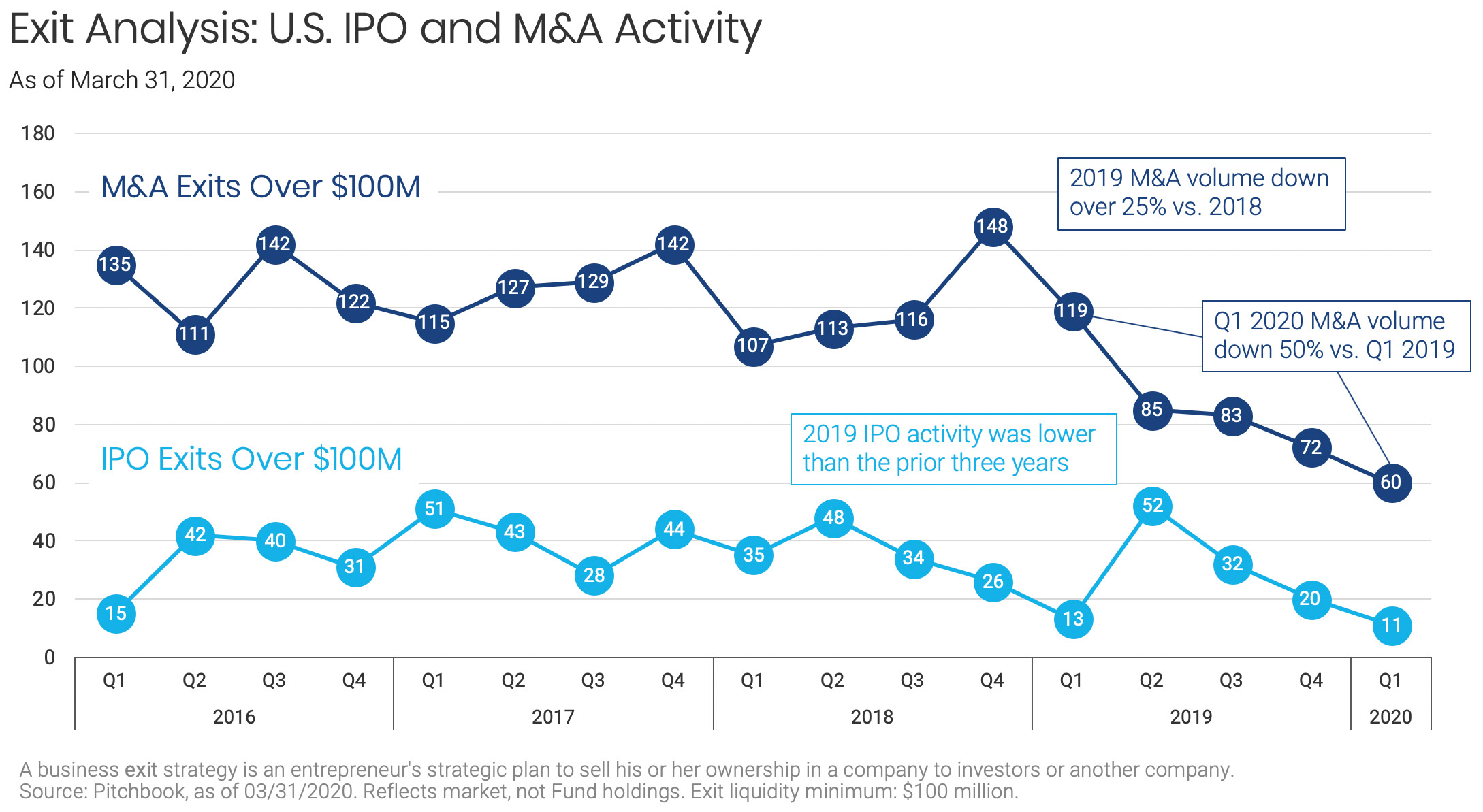

For the full year 2019, M&A volume (transactions over $100M) was down over 25% from the prior year. IPO activity in 2019 was also down to the lowest levels we have seen in years. First quarter of 2020 continued this trend (which was further exacerbated by the COVID-19 pandemic), with M&A volume (over $100M) down 49% compared to the first quarter of 2019—levels that we haven't seen in several years. Again, these trends predate the Coronavirus outbreak, so it's reasonable to assume that they may continue throughout 2020, especially now with the increased market volatility.

In terms of the 2020 exit environment (factors that influence a company’s exit), it is quite possible that both M&A and IPOs will be postponed and/or renegotiated, although there will always be exceptions. For private companies that were relying on near-term liquidity driven by factors including investor fatigue and the need for a public market currency, this environment can clearly have negative implications and may result in M&A transactions at distressed valuation levels. For companies with strong operating models, healthy balance sheets, and more patient investors, the likely impact would be an exit delay and willingness to stay private for longer until the opportune time arises to optimize liquidity. As shown previously, there had already been a diminished exit environment over the past few quarters before the Coronavirus outbreak was even reported. Historically, the combination of private company valuations being reined in and a pullback in the exit environment often led to dislocations, which created better pricing opportunities for sophisticated investors to buy private companies as sellers tended to become less price sensitive, particularly for these illiquid assets, and companies that were previously difficult to access became more available.

For that reason, some of the best performing vintages for private equity and venture capital funds fell during and immediately following years of increased market volatility and macro uncertainty. Again, we are not conflating the loss of life with financial returns, but those of us that have experienced highly volatile market cycles during periods of increased macroeconomic uncertainty understand that these tended to be attractive times to invest. When the public market had a pullback of more than 10% in 2016, the Fund added companies that resulted in some of our best exits to date. Thus, markets like this may provide good entry points for the Fund to invest in high-quality companies at attractive prices. Past performance is no guarantee of future results.

We are excited about the companies in our portfolio and the potential opportunities to both increase our positions in these companies at plausibly lower prices as well as to invest in new high-quality companies at attractive prices. While that is not to say these companies won’t face challenges due to various health and economic pressures in this environment, we do believe that they have differentiated business models, are operated by seasoned management teams, are backed by some of the best VCs, and have strong balance sheets to help manage through difficult cycles.

While our portfolio is not immune to what may happen over a sustained cycle like the one we are currently experiencing, we do have a number of companies that can potentially thrive in these economic conditions given capabilities around areas such as business continuity, online education, supply chain optimization, ecommerce, cloud, data analytics, and digital health. In our view, we believe the bigger implication will be that companies planning to raise capital over the next few quarters will face greater pressure on valuation and terms, and companies that were planning to exit may have a protracted time to exit until things settle down.

Historically, the Fund’s NAV has been relatively stable during periods of public market stress like those in 2016 and 2018, where we were able to invest in some very strong names at attractive prices. Currently, the Fund has a robust pipeline of opportunities and we will continue investing through this cycle while maintaining discipline, relying upon our robust diligence process, and leveraging our relationships across the ecosystem.

1 Burn rate is the rate at which a new company is spending its venture capital to finance overhead before generating positive cash flow from operations.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus with this and other information about The Private Shares Fund (the "Fund"), please download here, or call 1-855-551-5510. Read the prospectus carefully before investing.

The investment minimums are $2,500 for the Class A Share and Class L Share, and $1,000,000 for the Institutional Share

Investment in the Fund involves substantial risk. The Fund is not suitable for investors who cannot bear the risk of loss of all or part of their investment. The Fund is appropriate only for investors who can tolerate a high degree of risk and do not require a liquid investment. The Fund has no history of public trading and investors should not expect to sell shares other than through the Fund's repurchase policy regardless of how the Fund performs. The Fund does not intend to list its shares on any exchange and does not expect a secondary market to develop.

All investing involves risk including the possible loss of principal. Shares in the Fund are highly illiquid, and can be sold by shareholders only in the quarterly repurchase program of the Fund which allows for up to 5% of the Fund's outstanding shares at NAV to be redeemed each quarter. Due to transfer restrictions and the illiquid nature of the Fund's investments, you may not be able to sell your shares when, or in the amount that, you desire. The Fund intends to primarily invest in securities of private, late-stage, venture-backed growth companies. There are significant potential risks relating to investing in such securities. Because most of the securities in which the Fund invests are not publicly traded, the Fund's investments will be valued by Liberty Street Advisors, Inc. (the "Investment Adviser") pursuant to fair valuation procedures and methodologies adopted by the Board of Trustees. While the Fund and the Investment Adviser will use good faith efforts to determine the fair value of the Fund's securities, value will be based on the parameters set forth by the prospectus. As a consequence, the value of the securities, and therefore the Fund's Net Asset Value (NAV), may vary.

There are significant potential risks associated with investing in venture capital and private equity-backed companies with complex capital structures. The Fund focuses its investments in a limited number of securities, which could subject it to greater risk than that of a larger, more varied portfolio. There is a greater focus in technology securities that could adversely affect the Fund’s performance. The Fund's quarterly repurchase policy may require the Fund to liquidate portfolio holdings earlier than the Investment Adviser would otherwise do so and may also result in an increase in the Fund's expense ratio. Portfolio holdings of private companies that become publicly traded likely will be subject to more volatile market fluctuations than when private, and the Fund may not be able to sell shares at favorable prices, such companies frequently impose lock-ups that would prohibit the Fund from selling shares for a period of time after an initial public offering (IPO). Market prices of public securities held by the Fund may decline substantially before the Investment Adviser is able to sell the securities.

The Fund may invest in private securities utilizing special purpose vehicles ("SPV"s), private investment funds (“Private Funds”), private investments in public equity ("PIPE") transactions where the issuer is a special purpose acquisition company ("SPAC"), and profit sharing agreements. The Fund will bear its pro-rata portion of expenses on investments in SPVs, Private Funds, or similar investment structures and will have no direct claim against underlying portfolio companies. PIPE transactions involve price risk, market risk, expense risk, and the Fund may not be able to sell the securities due to lock-ups or restrictions. Profit sharing agreements may expose the Fund to certain risks, including that the agreements could reduce the gain the Fund otherwise would have achieved on its investment, may be difficult to value and may result in contractual disputes. Certain conflicts of interest involving the Fund and its affiliates could impact the Fund’s investment returns and limit the flexibility of its investment policies. This is not a complete enumeration of the Fund's risks. Please read the Fund prospectus for other risk factors related to the Fund.

The Fund may not be suitable for all investors. Investors are encouraged to consult with appropriate financial professionals before considering an investment in the Fund.

Companies that may be referenced on this website are privately-held companies. Shares of these privately-held companies do not trade on any national securities exchange, and there is no guarantee that the shares of these companies will ever be traded on any national securities exchange.

The Private Shares Fund is distributed by FORESIDE FUND SERVICES, LLC

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus with this and other information about The Private Shares Fund (the "Fund"), please download here, or call 1-855-551-5510. Read the prospectus carefully before investing.

The investment minimums are $2,500 for the Class A Share and Class L Share, and $1,000,000 for the Institutional Share

Investment in the Fund involves substantial risk. The Fund is not suitable for investors who cannot bear the risk of loss of all or part of their investment. The Fund is appropriate only for investors who can tolerate a high degree of risk and do not require a liquid investment. The Fund has no history of public trading and investors should not expect to sell shares other than through the Fund's repurchase policy regardless of how the Fund performs. The Fund does not intend to list its shares on any exchange and does not expect a secondary market to develop.

All investing involves risk including the possible loss of principal. Shares in the Fund are highly illiquid, and can be sold by shareholders only in the quarterly repurchase program of the Fund which allows for up to 5% of the Fund's outstanding shares at NAV to be redeemed each quarter. Due to transfer restrictions and the illiquid nature of the Fund's investments, you may not be able to sell your shares when, or in the amount that, you desire. The Fund intends to primarily invest in securities of private, late-stage, venture-backed growth companies. There are significant potential risks relating to investing in such securities. Because most of the securities in which the Fund invests are not publicly traded, the Fund's investments will be valued by Liberty Street Advisors, Inc. (the "Investment Adviser") pursuant to fair valuation procedures and methodologies adopted by the Board of Trustees. While the Fund and the Investment Adviser will use good faith efforts to determine the fair value of the Fund's securities, value will be based on the parameters set forth by the prospectus. As a consequence, the value of the securities, and therefore the Fund's Net Asset Value (NAV), may vary.

There are significant potential risks associated with investing in venture capital and private equity-backed companies with complex capital structures. The Fund focuses its investments in a limited number of securities, which could subject it to greater risk than that of a larger, more varied portfolio. There is a greater focus in technology securities that could adversely affect the Fund’s performance. The Fund's quarterly repurchase policy may require the Fund to liquidate portfolio holdings earlier than the Investment Adviser would otherwise do so and may also result in an increase in the Fund's expense ratio. Portfolio holdings of private companies that become publicly traded likely will be subject to more volatile market fluctuations than when private, and the Fund may not be able to sell shares at favorable prices, such companies frequently impose lock-ups that would prohibit the Fund from selling shares for a period of time after an initial public offering (IPO). Market prices of public securities held by the Fund may decline substantially before the Investment Adviser is able to sell the securities.

The Fund may invest in private securities utilizing special purpose vehicles ("SPV"s), private investment funds (“Private Funds”), private investments in public equity ("PIPE") transactions where the issuer is a special purpose acquisition company ("SPAC"), and profit sharing agreements. The Fund will bear its pro-rata portion of expenses on investments in SPVs, Private Funds, or similar investment structures and will have no direct claim against underlying portfolio companies. PIPE transactions involve price risk, market risk, expense risk, and the Fund may not be able to sell the securities due to lock-ups or restrictions. Profit sharing agreements may expose the Fund to certain risks, including that the agreements could reduce the gain the Fund otherwise would have achieved on its investment, may be difficult to value and may result in contractual disputes. Certain conflicts of interest involving the Fund and its affiliates could impact the Fund’s investment returns and limit the flexibility of its investment policies. This is not a complete enumeration of the Fund's risks. Please read the Fund prospectus for other risk factors related to the Fund.

The Fund may not be suitable for all investors. Investors are encouraged to consult with appropriate financial professionals before considering an investment in the Fund.

Companies that may be referenced on this website are privately-held companies. Shares of these privately-held companies do not trade on any national securities exchange, and there is no guarantee that the shares of these companies will ever be traded on any national securities exchange.

The Private Shares Fund is distributed by FORESIDE FUND SERVICES, LLC